Residential Property Review – March 2020

SPRING BUDGET: WHAT DOES IT MEAN FOR THE HOUSING MARKET?

While it is true that this year’s highly anticipated Spring Budget speech, delivered by new Chancellor Rishi Sunak, was understandably dominated by the government’s emergency measures to protect the British economy and population from the impact of COVID-19, there were other positives to be gleaned on the future of the housing market.

In addition to the support measures introduced for homeowners struggling financially in the wake of the crisis, Mr Sunak also announced that the government would be making the provision of affordable and social housing a priority, earmarking £12bn in funding for the extension of the Affordable Home Programme. He also said that he would be cutting interest rates on lending for social housing by one percentage point, unlocking over £1bn of discounted loans for investment in local infrastructure.

Furthermore, the Chancellor committed £1.1bn to the construction of almost 70,000 new homes in areas of high demand.

Prospective homebuyers awaiting comprehensive Stamp Duty Land Tax (SDLT) reform were disappointed, however. While the Chancellor announced the introduction of a 2% SDLT surcharge for

overseas buyers of UK residential properties, no other Stamp Duty reforms were forthcoming.

THREE-MONTH ‘MORTGAGE HOLIDAY’ FOR STRUGGLING HOMEOWNERS

As the COVID-19 pandemic hits businesses up and down the country, employees have faced reduced income and redundancy, as their employers struggle for survival. The Chancellor’s announcement that high street lenders would be introducing a three-month mortgage holiday for those affected financially by the crisis, should be some comfort for borrowers.

Just a few days after a raft of complaints from organisations and bodies representing the interests of private renters, for whom no financial protection had initially been announced, the government introduced legislation banning landlords from evicting tenants for a period of three months and extended mortgage payment holidays to buy-to-let mortgages.

BOE SLASHES BASE RATE TO RECORD LOW

On Wednesday 11 March, the Bank of England (BoE) took the unprecedented action of cutting the base rate from 0.75% to 0.25% to provide relief to families and small businesses struggling under the financial impact of the pandemic.

Just a week later, the decision was made to slash interest rates to their lowest ever level – 0.1% – as the sheer scale of the economic havoc wrought by the virus became clearer.

The Governor of the BoE, Andrew Bailey, commented: “The obvious increase in the pace and severity of Covid-19, which has built during the week, was something we had to assess and respond to, we can’t wait for the hard economic data before we act.”

| The Chancellor’s announcement that high street lenders would be introducing a three-month mortgage holiday for those affected financially by the crisis, should be some comfort for borrowers. |

House Prices Headline statistics

| HOUSE PRICE INDEX (JAN 2020)* | 121.3* |

| Average House Price | £231,185 |

| Monthly Change | -1.2% |

| Annual Change | 1.3% |

*(Jan 2015 = 100)

- UK house prices increased by 1.3% in the year to January 2020, down from 1.7% in December 2019

- On a non-seasonally adjusted basis, average house prices in the UK decreased by 1.1% between December 2019 and January 2020

- This is compared with a fall of 0.6% during the same period a year earlier

House Prices Price change by region

Source: The Land Registry AVERAGE MONTHLY PRICE BY PROPERTY TYPE – JAN 2020

Source: The Land Registry

|

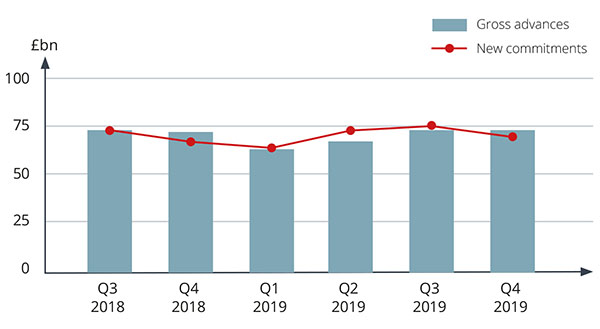

Mortgage Activity

- The value of gross mortgage advances was £73.4 bn in 2019 Q4

- This is broadly unchanged in comparison to 2018 Q4

Source: FCA & Bank of England

It is important to take professional advice before making any decision relating to your personal finances. Information within this document is based on our current understanding and can be subject to change without notice and the accuracy and completeness of the information cannot be guaranteed. It does not provide individual tailored investment advice and is for guidance only. Some rules may vary in different parts of the UK. We cannot assume legal liability for any errors or omissions it might contain. Levels and bases of, and reliefs from, taxation are those currently applying or proposed and are subject to change; their value depends on the individual circumstances of the investor. No part of this document may be reproduced in any manner without prior permission.