Property Market Review – August 2020

TRUE IMPACT OF THE PANDEMIC YET TO BE FELT

According to Derwent London (property investor, developer and landlord in the capital), the real impact of the pandemic on the office market is yet to be felt. With job losses and business failures likely to increase over the next few months, office vacancies will also rise and place pressure on rents, which look likely to fall as a result.

Focusing on office occupancy levels, Paul Williams, Derwent’s Chief Executive, is not expecting workplaces to reach beyond 50% of capacity over the next few months. Despite this, some demand for new office space in the capital has been noted, from firms including Slaughter and May, and Netflix. Evidence suggests that occupiers’ priorities have re-positioned. Mr Williams, commented: “They are saying they want more space available: less hotdesking, less packing [people in], less sedentary desk space; more collaborative space.”

UK RETAIL RECOVERY UNLIKELY FOR SOME TIME

The most recent ‘UK Retail Monitor’ from Knight Frank for Q2 2020, highlights the continued plight of the retail sector in the UK. Closure of all but essential retail, understandably caused sharp declines in values and volumes. Interestingly, high streets and shopping centres experienced footfall declines between -88% and -65%, but due to their accessibility by car and large store formats facilitating social distancing, retail parks experienced lesser footfall declines (April -63%, May -55% and June -34%). Consumer confidence fell sharply between Q1 and Q2 2020 (-34), with only a marginal recovery (-27) by the end of Q2.

Knight Frank feel that the effects of the pandemic will continue to ‘unravel‘ during the second half of the year, with any ‘meaningful recovery‘ in retail properties unlikely until 2021, or into 2022. Stephen Springham, Head of Retail Research at Knight Frank, concluded: “Q2 saw some of the worst retail statistics on record, illustrating the crippling effects of COVID-19 and subsequent lockdown. Relaxation of restrictions occurred just over a week before quarter-end in England and NI and has thus far brought little respite.”

INDUSTRIAL SECTOR STILL DISPLAYS RESILIENCE

Although rental expectations over the next twelve-month period for prime and secondary office space, and primary and secondary retail rents, are negative, the recently released UK Commercial Property Survey for Q2 2020, highlights that sentiment is much more resilient across the industrial sector. Despite rents in secondary locations falling by around -1% in the next 12 months, prime industrial rents continue to display a positive outlook, with respondents to the quarterly survey anticipating growth of just under 2% over the next year. This outperformance for the industrial sector is evident in respondents’ expectations at both regional and national level.

From a commercial property investment perspective, survey respondents reported a fall in investor enquiries during the second quarter of the year (-46%), the weakest return for this indicator since the end of August 2008 and down from a figure of -14% in Q1 2020. At a sector breakdown level, demand is declining in every area of the market, but it is reported that conditions in the industrial sector are ‘less downbeat’ than those in both the retail and the office sectors.

| With job losses and business failures likely to increase over the next few months, office vacancies will also rise and place pressure on rents, which look likely to fall as a result. |

COMMERCIAL PROPERTY CURRENTLY FOR SALE IN THE UK

![]()

- Regions with the highest number of commercial properties for sale currently are the South West and North West of England

- Northern Ireland currently has the lowest number of commercial properties for sale (33 properties)

- There are currently 1,237 commercial properties for sale in London, the average asking price is £1,064,402

Source: Zoopla, data extracted 20 August 2020

| REGION | NO. PROPERTIES | AVG. ASKING PRICE |

|---|---|---|

| LONDON | 1,237 | £1,064,402 |

| SOUTH EAST ENGLAND | 1,358 | £574,461 |

| EAST MIDLANDS | 992 | £853,918 |

| EAST OF ENGLAND | 825 | £475,793 |

| NORTH EAST ENGLAND | 981 | £307,200 |

| NORTH WEST ENGLAND | 1,857 | £401,299 |

| SOUTH WEST ENGLAND | 1,842 | £632,368 |

| WEST MIDLANDS | 1,306 | £461,505 |

| YORKSHIRE AND THE HUMBER | 1,393 | £367,658 |

| ISLE OF MAN | 52 | £479,025 |

| SCOTLAND | 1,362 | £267,100 |

| WALES | 847 | £380,700 |

| NORTHERN IRELAND | 33 | £427,873 |

COMMERCIAL PROPERTY OUTLOOK

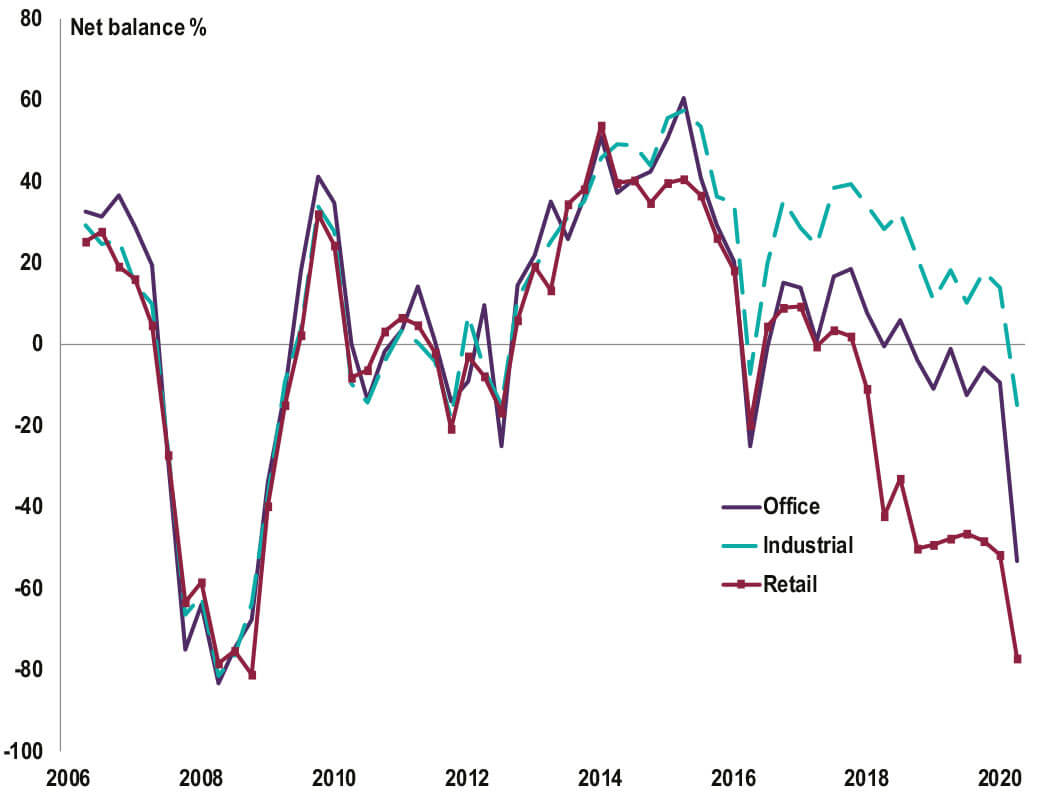

INVESTMENT ENQUIRIES – BROKEN DOWN BY SECTOR

- A headline net balance of -46% reported a fall in enquiries during Q2

- Down from -14% in Q1 and the weakest return for this indicator since the end of 2008

- Conditions in the industrial sector are less downbeat than retail and office sectors

Source: RICS, UK Commercial Property Market Survey, Q2 2020

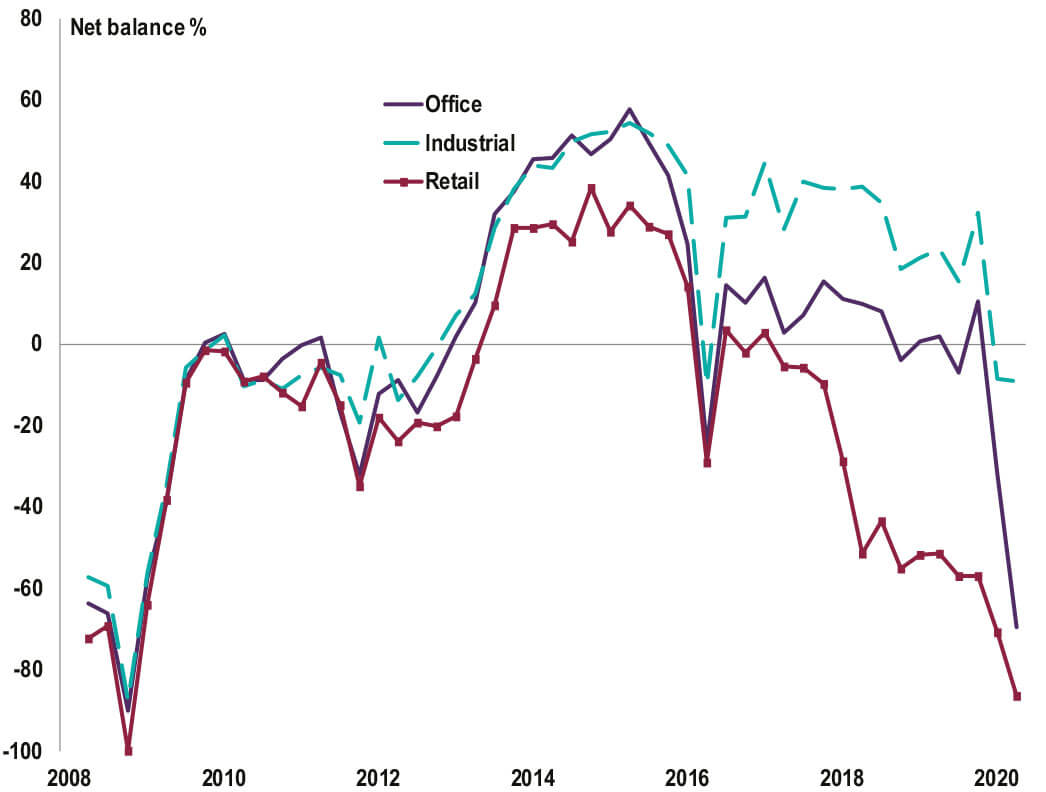

CAPITAL VALUE EXPECTATIONS – BROKEN DOWN BY SECTOR

- Twelve-month capital value expectations are firmly negative

for retail units and offices - Prime industrial capital values are still seen posting

marginal gains in the year ahead, although the outlook is

slightly negative for secondary

Source: RICS, UK Commercial Property Market Survey, Q2 2020

All details are correct at the time of writing (20 August 2020)

It is important to take professional advice before making any decision relating to your personal finances. Information within this document is based on our current understanding and can be subject to change without notice and the accuracy and completeness of the information cannot be guaranteed. It does not provide individual tailored investment advice and is for guidance only. Some rules may vary in different parts of the UK. We cannot assume legal liability for any errors or omissions it might contain. Levels and bases of, and reliefs from, taxation are those currently applying or proposed and are subject to change; their value depends on the individual circumstances of the investor. No part of this document may be reproduced in any manner without prior permission.